Most people have heard of Fannie Mae and Freddie Mac. But many, even in the housing business, are not entirely certain what role they play. Fannie Mae was initially established by Congress during the Great Depression to help improve access to mortgage credit (Freddie Mac was set-up later in the 1970s). Fannie and Freddie do not make mortgage loans to individual borrowers like you and me. Rather, they operate in the “secondary” market, buying home mortgages initially originated by banks. This system frees up capital so that banks can lend additional mortgage loans, thus providing “liquidity” to the market.

Today, Fannie and Freddie are private companies and are among the largest corporations in the world. By some estimates, these two companies hold nearly half of all U.S. mortgages and have assets in the trillions of dollars. But Fannie and Freddie’s business in rural communities is less substantial. Between 2012 and 2015, the mortgage giants’ rural loan activity accounted for roughly 12 percent of their total purchases – less than the overall rate of mortgage originations in rural areas.

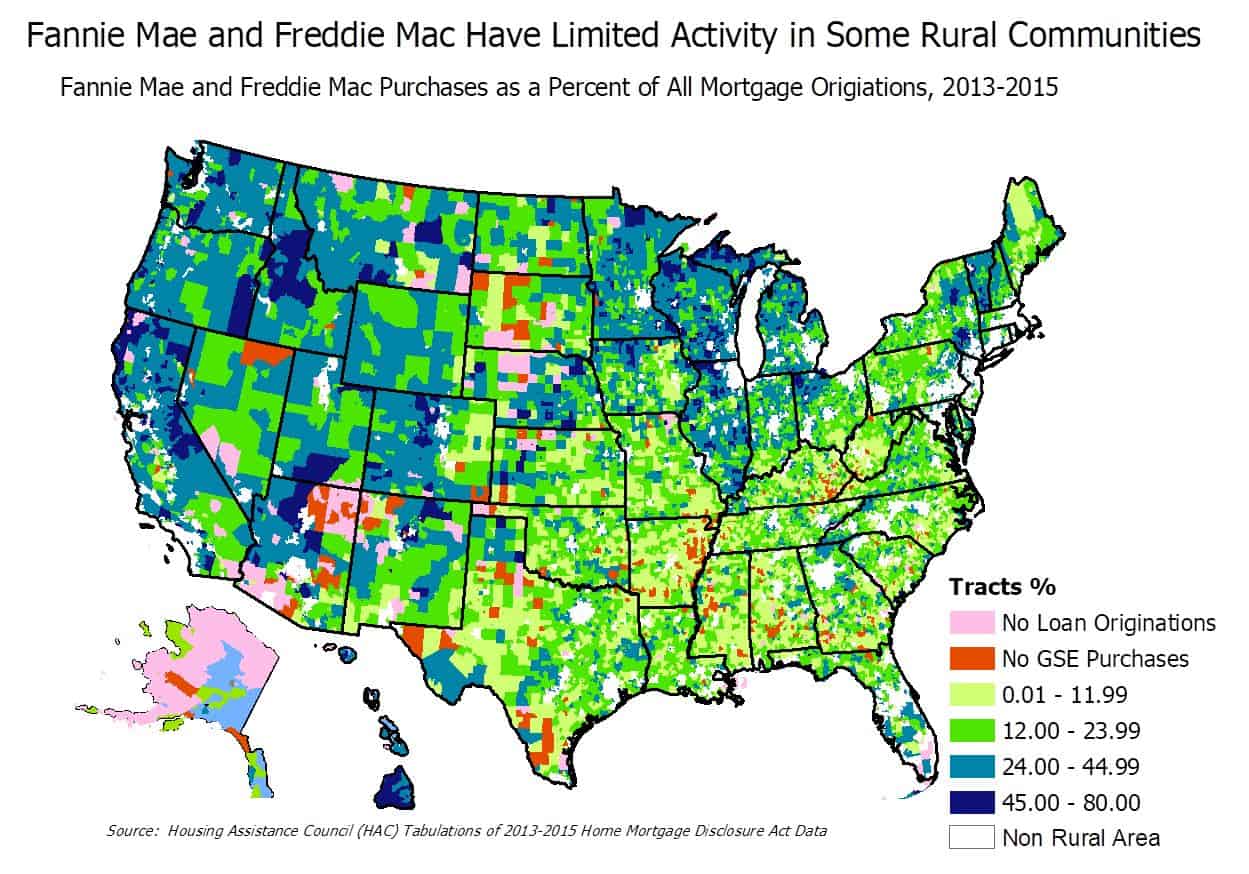

A closer look at Fannie and Freddie’s activity within rural markets reveals even greater discrepancies. Generally, the more rural a community, the less likely Fannie or Freddie purchased a loan there, and their rural activity is concentrated near suburban and urban areas.[i] Mortgage dollars often flow to suburban and more urbanized communities for a number of reasons, ranging from higher incomes to greater access to financial services[ii] In some rural markets, the two companies have minimal to nonexistent purchase activity, notably rural areas with low incomes, high poverty, and minority populations. The map below indicates the level of Fannie Mae and Freddie Mac’s rural activity from 2012-2014. The areas with absolutely no mortgages are most often associated with remote rural areas or Native American lands. Similarly, Freddie Mac’s mortgage activity in high need rural areas actually declined for each of the past two years.[iii]

A Duty to Serve Underserved Markets

In response to the uneven (and inadequate) flow of mortgage dollars to rural communities, Congress stepped in and is requiring Fannie and Freddie to increase their business in rural markets. The new regulations require the companies to increase their mortgage activity in high needs rural areas and populations, work with small banks to finance more housing, and help preserve rental housing. After a lengthy delay due the financial crisis, as well as Fannie and Freddie’s own financial health, the new rules are finally being implemented, and took effect on January 1, 2018.

The rural-specific component may be the broadest and most challenging of the Duty to Serve tasks. At the core of both company’s plans is to buy more mortgages in rural areas. For example, Fannie Mae’s goal is to purchase 13,500 loans in rural high need areas annually by 2020. Some elements of the plans are more controversial, such as allowing the companies to re-enter the Low-Income Housing Tax Credit market – a business line from which the companies have been prohibited since their placement in conservatorship in 2008.

In many respects, Fannie and Freddie’s current products are not particularly well-suited for many rural markets, as evidenced by their low activity and the congressional mandate itself. New and creative approaches are needed to fully achieve their goals in rural areas. The most effective approach would be for Fannie and Freddie to partner with existing housing providers, nonprofits, and tribes, who already work in these communities. These entities have the experience, local trust, and insights to help Fannie and Freddie in these often hard to reach areas. Ultimately, rural America is a big place, with many different housing markets. To make this plan a success, Fannie and Freddie will need to better understand these often-forgotten markets, and commit meaningful efforts and investment.

To read Fannie Mae’s and Freddie Mac’s plans for rural America visit:

Rural “housers” will be watching.

Lance George is the director of research and information at the Housing Assistance Council (HAC). HAC is a national nonprofit organization that helps build homes and communities across rural America. For more information, contact Lance at lance@ruralhome.org.

[i] Housing Assistance Council Tabulations of 2012-2015 Home Mortgage Disclosure Act data.

[ii] Housing Assistance Council Comments on the Duty to Serve Final Rule. http://www.ruralhome.org/storage/documents/policy_comments/dts/HAC_Duty_To_Serve_Comments_3_17_16.pdf

[iii]Freddie Mac Duty to Serve Proposed Plan. Page 36. https://www.fhfa.gov/PolicyProgramsResearch/Programs/Documents/FreddieProposedUMP.pdf

![]()